One of the most common questions we hear from buyers is:

- “How much home can I actually afford?”

And while it seems like a simple question, the answer is often misunderstood.

Because what a lender says you can afford and what you should comfortably afford are not always the same thing.

Why Affordability Is About More Than Just Approval

When you get pre-approved, a lender gives you a maximum loan amount based on your finances.

But that number doesn’t always reflect your real-life lifestyle.

According to the Consumer Financial Protection Bureau, affordability should take into account your full financial picture—not just your loan limit. Affordability is not just about the highest loan amount a lender may approve. The CFPB explains that buyers should estimate what they can comfortably afford by looking at monthly payment, down payment, interest rate, taxes, insurance, and loan terms together. This is why your “comfortable number” may be lower than your maximum approval, especially if you want room for savings, emergencies, and everyday life.

💡 Real-life insight:

We’ve worked with buyers who were approved for $300,000 but chose to stay closer to $250,000 to keep their monthly budget comfortable.

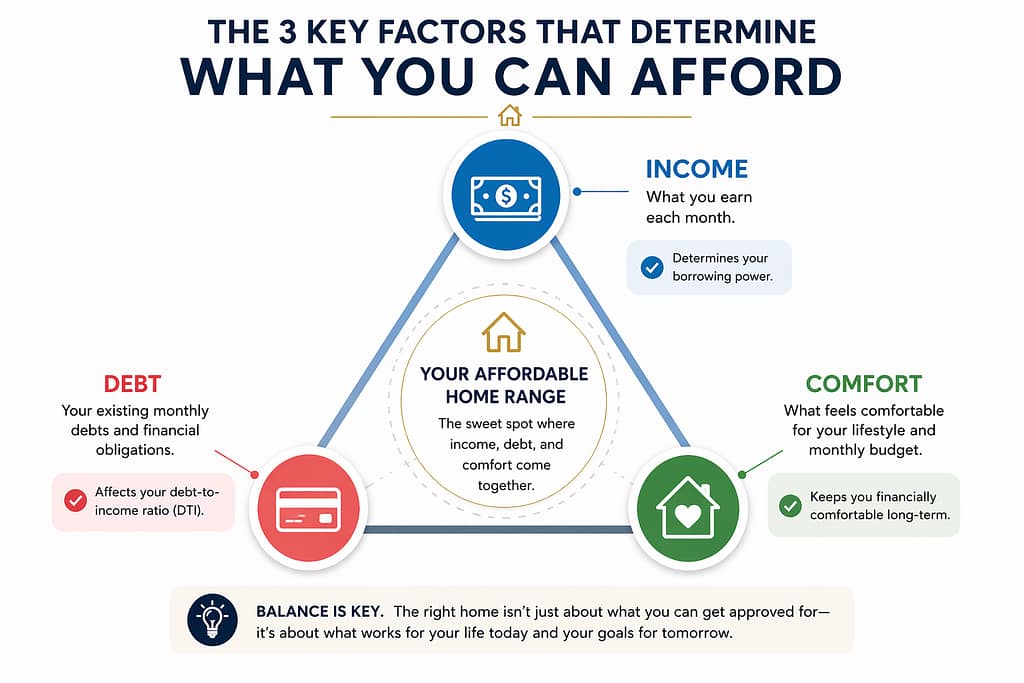

The 3 Numbers That Determine What You Can Afford

A realistic home budget usually starts with how much you can comfortably pay each month, how much you can put toward a down payment, the type of loan you choose, and the interest rate and terms attached to that loan. The CFPB notes that changing any one of these factors can change the price range you may be able to afford. That makes affordability more flexible than just looking at one approved number. 1

Instead of focusing only on the home price, focus on these three key factors:

Your Income

- Your income determines your starting point.

- Lenders use it to calculate how much you can borrow, but it also helps you decide what monthly payment feels manageable.

Your Debt

This includes:

- Car payments

- Credit cards

- Student loans

Lenders calculate your debt-to-income ratio (DTI) to measure how much of your income is already committed. Debt-to-income ratio, or DTI, compares your monthly debt payments to your gross monthly income. Lenders use this number to understand how much of your income is already committed before adding a mortgage payment. A lower DTI can make a borrower look stronger because it suggests there is more room in the budget to manage a new home loan. 2

Your Monthly Comfort Level

This is the most overlooked factor.

Ask yourself:

- “What monthly payment would feel comfortable—not stressful?”

Because homeownership should add stability, not pressure.

What Lenders Say You Can Afford vs What You Should Spend

This is where many buyers get tripped up.

| Category | Lender Perspective | Your Perspective |

| Goal | Max approval | Comfortable living |

| Focus | Numbers | Lifestyle |

| Flexibility | Limited | Personal choice |

A lender’s approval is based on financial criteria, but your personal comfort level should also guide the decision. The CFPB recommends treating affordability estimates as a starting point, not a final answer, because assumptions can change as you learn more about taxes, insurance, rates, and loan options. This supports the idea that buyers do not have to spend their maximum approval just because they qualify for it.

- Just because you’re approved for a higher amount doesn’t mean you should spend it.

Breaking Down a Real Monthly Payment (PITI)

Your mortgage payment includes more than just the loan.

It’s made up of:

- Principal (loan amount)

- Interest (cost of borrowing)

- Taxes (property taxes)

- Insurance (homeowners insurance)

This is known as PITI. It stands for principal, interest, taxes, and insurance, which are the main parts of a typical monthly mortgage payment. Principal and interest are tied to the loan itself, while taxes and insurance are ongoing ownership costs that can affect the total monthly payment. Understanding PITI helps avoid surprises when budgeting, and helps you estimate the full cost of homeownership instead of budgeting only for the loan amount. 3

The CFPB explains that principal and interest are calculated using the loan amount, loan term, and interest rate. However, the total payment sent to the mortgage company is often higher because it may also include homeowners insurance and property taxes. This is why two homes with similar prices can still have different monthly payments depending on tax rates, insurance costs, and loan structure. 4

Example: What Different Budgets Look Like in Central Texas

Here’s a simplified look:

| Home Price | Estimated Monthly Payment |

| $200,000 | ~$1,300–$1,500 |

| $250,000 | ~$1,600–$1,900 |

| $300,000 | ~$1,900–$2,300 |

Payment examples are helpful as a starting point, but they should never be treated as exact quotes. The CFPB notes that affordability estimates depend on assumptions such as interest rate, down payment, loan type, and taxes or insurance. Buyers should use examples to understand the relationship between price and payment, then confirm the real numbers with a lender. 5

💡 Important:

These numbers vary based on interest rates, taxes, and loan type—but they give a helpful starting point.

Hidden Costs Buyers Often Forget

This is where many first-time buyers get surprised.

Beyond your mortgage, you may also have:

- Maintenance and repairs

- Utilities

- HOA fees (if applicable)

- Moving costs

Some costs of homeownership do not show up in the loan amount, but they still affect monthly life. The CFPB encourages buyers to estimate property taxes and homeowners insurance when calculating affordability, and other expenses like utilities, maintenance, HOA fees, and moving costs should also be considered in a realistic budget. This helps buyers avoid becoming house-rich but cash-stretched.

- These don’t show up in your loan—but they affect your monthly life.

How to Find Your Comfortable Price Range

Here’s a simple approach:

- Start with your pre-approval

- Look at your monthly budget

- Factor in lifestyle expenses

- Leave room for savings and flexibility

A smart affordability range should begin with pre-approval, but it should be refined using your real monthly budget. The CFPB suggests subtracting estimated taxes and insurance from your target total monthly home payment to understand how much you can afford for principal and interest. This gives buyers a clearer and more realistic price range before they start shopping seriously.

💡 Pro tip:

The right home price is one that allows you to live comfortably—not just qualify.

Final Thoughts: Buy Smart, Not Just Approved

Understanding how much home you can afford isn’t just about numbers—it’s about creating a lifestyle that feels stable, manageable, and aligned with your long-term goals. While getting pre-approved gives you a helpful starting point, it doesn’t define what’s best for you. The real goal is finding a price range that allows you to enjoy your home without feeling financially stretched.

Most buyers are surprised to learn that they have more control in this decision than they initially thought. You’re not required to spend your maximum approval, and in many cases, choosing a slightly lower price point can create more flexibility for everyday life, savings, and unexpected expenses.

This is where having the right guidance makes a meaningful difference. At Twins Realty Group, we help you look at both sides of the equation. One twin works with you on the mortgage side to clearly understand your numbers, while the other helps you navigate the market and find a home that fits both your needs and your budget. This approach keeps everything aligned, so you’re not just buying a home—you’re making a decision that works for your life.

If you’re starting to explore what’s possible or want help understanding your numbers, we’re here to guide you through it step by step. One twin handles the loan, one secures the home, and together, we create one smooth and confident experience from start to finish.