One of the biggest concerns buyers have today is:

- “How much do interest rates actually matter?”

And the answer is:

- A lot more than most people realize.

Even small changes in mortgage interest rates can significantly affect:

- Your monthly payment

- Your affordability

- The price range you qualify for

Understanding how rates impact buying power can help you make smarter decisions and avoid focusing only on the home price itself.

Why Interest Rates Matter More Than Most Buyers Realize

Many buyers focus mainly on:

- Purchase price

- Down payment

- Monthly budget

But interest rates directly affect how expensive borrowing money becomes over time.

Interest rates affect both the monthly payment and the total amount a buyer pays over the life of the loan. According to the Consumer Financial Protection Bureau1, the rate is important, but buyers should also compare fees, points, mortgage insurance, and closing costs when reviewing loan options. This is why focusing only on the home price can give buyers an incomplete picture of affordability.

- This means even a 1% rate difference can have a major long-term impact.

What Is a Mortgage Interest Rate?

A mortgage interest rate is the percentage a lender charges you for borrowing money to purchase a home. Several personal and market-related factors can influence the mortgage rate a buyer receives.

The CFPB2 list down seven factors that influence your mortgage interest; these are:

- Credit score

- Home price and Loan amount

- Down payment

- Loan Term

- Interest rate type

- Loan Type

- Location

- Lower rates generally mean lower monthly payments.

Understanding these factors helps buyers see which parts they may be able to improve before applying.

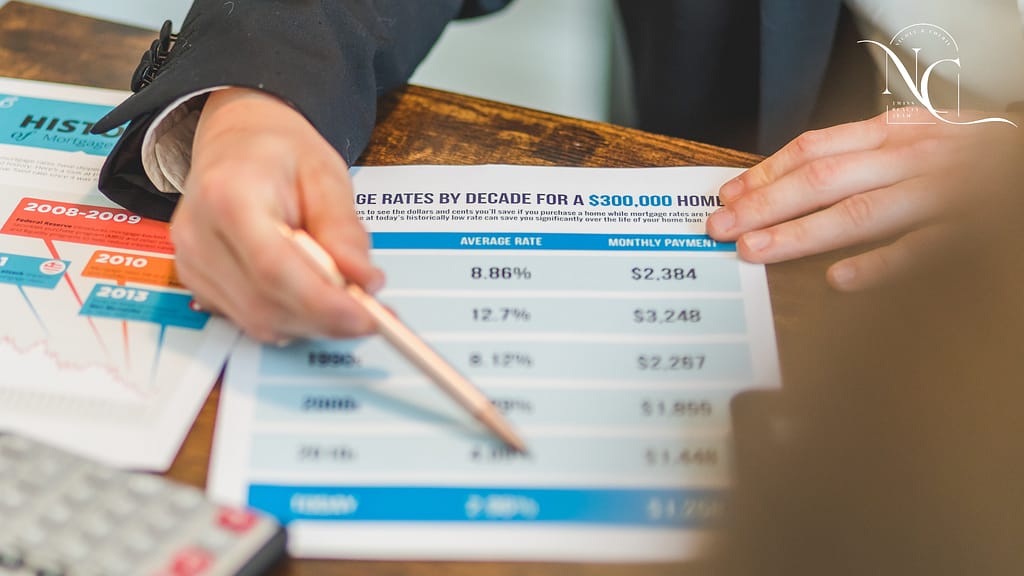

How Interest Rates Affect Monthly Payments

As interest rates increase:

- Monthly mortgage payments also increase.

Here’s a simplified example on a 30-year fixed mortgage:

| Loan Amount | Interest Rate | Estimated Principal & Interest |

|---|---|---|

| $300,000 | 5% | Lower monthly payment |

| $300,000 | 7% | Higher monthly payment |

Even though the home price stays the same, the monthly cost changes significantly. When interest rates rise, the same loan amount becomes more expensive because more of the payment goes toward interest. Rocket Mortgage3 explains that mortgage interest is the cost of borrowing money from the lender, and it is calculated as part of the borrower’s monthly payment. This is why two buyers purchasing homes at the same price can have very different payments if their interest rates are different.

How Higher Rates Reduce Buying Power

Buying power refers to:

- How much home you can comfortably afford.

When rates rise:

- Monthly payments increase

- Loan qualification amounts may decrease

- Buyers may need to lower their price range

💡 Example:

A buyer approved at a lower rate may qualify for a more expensive home than they would at a higher rate.

Higher mortgage rates can reduce buying power because they increase the monthly cost of borrowing. A study by the Texas Real Estate Research Center4 explains that as rates rise, home-purchasing affordability declines, meaning buyers may need to lower their price range to keep payments manageable. This is especially important in markets where buyers are already balancing home prices, taxes, and insurance costs.

Should You Wait for Rates to Drop?

This is one of the most common questions buyers ask.

The challenge is:

- No one can predict interest rates perfectly.

And waiting can sometimes create new challenges:

- Higher home prices

- Increased competition

- Reduced inventory

In some cases, buyers who wait for lower rates may end up paying more for the home itself. Waiting for rates to drop can feel logical, but it is not always predictable or risk-free. Freddie Mac’s5 weekly mortgage survey shows that rates can move up or down over time based on broader market conditions, and buyers cannot perfectly control when those changes happen. Because of this, it is often smarter to evaluate your readiness, payment comfort, and available homes instead of making decisions based only on rate predictions.

Interest Rates vs Home Prices: The Bigger Picture

Mortgage decisions shouldn’t focus only on rates.

You also need to consider:

- Home prices

- Inventory levels

- Personal financial readiness

- Long-term goals

- Sometimes buying at a slightly higher rate now may still make more sense than waiting indefinitely.

Mortgage affordability depends on both borrowing costs and home prices, not interest rates alone. Another study from Texas Real Estate Research Center6 notes that higher rates can affect affordability, but buyers also have to consider local prices, inventory, and household income. This is why the better question is not always “Are rates low?” but “Does this purchase make sense for my full financial picture?” (Texas Real Estate Research Center)

How Credit Scores Affect Your Interest Rate

Your credit score can significantly impact the rate you receive.

Generally:

- Higher credit scores may qualify for better rates

- Lower scores may increase borrowing costs

This is one reason improving your credit before buying can be so valuable. Credit score is one of the major borrower-specific factors that can affect mortgage pricing. Consumers with higher credit scores generally receive lower interest rates than consumers with lower scores because lenders use credit history to estimate repayment risk. Improving credit before applying can therefore help buyers strengthen their loan options.

Ways Buyers Can Improve Their Rate

Some strategies may include:

- Improving credit score

- Reducing debt

- Increasing down payment

- Comparing lenders

- Exploring different loan options

- Even small improvements can make a meaningful difference over time.

Buyers may not be able to control the broader market, but they can often improve parts of their own borrower profile. The CFPB recommends comparing offers from multiple lenders, reviewing loan estimates, and understanding how factors like credit score, down payment, loan type, and loan term affect the rate. These steps can help buyers find a more competitive loan instead of accepting the first option they receive.

Final Thoughts: Focusing on the Full Financial Picture

Interest rates are one of the biggest factors affecting affordability in today’s housing market, but they’re only one part of the bigger picture. While higher rates can increase monthly payments and reduce buying power, focusing only on rates without considering home prices, long-term goals, and personal readiness can lead to incomplete decisions.

Many buyers become discouraged when rates rise, but the reality is that market conditions are always changing. The right time to buy often depends more on your financial stability, future plans, and overall comfort level than trying to perfectly time interest rates. Understanding how rates impact your payment helps you make informed decisions instead of emotional ones.

At Twins Realty Group, we help buyers understand both the financial and practical side of the market. One twin helps guide you through loan options, affordability, and rate-related decisions, while the other helps you evaluate the market and find the right home for your goals. Together, we help you look beyond headlines and focus on what truly makes sense for your situation.

If you’re trying to understand how interest rates affect your buying power or wondering what your options look like in today’s market, we’re here to help you walk through it step by step. One twin handles the loan, one secures the home, and together, we help you make confident and informed home buying decisions.